BLS E-Services IPO Review – GMP, Financials and More

BLS E-Services IPO Review – GMP, Financials and More

[ad_1]

BLS E-Services IPO Review: BLS International Services is a nearly two-decade-old business enterprise that was born out of providing visa processing services way back in 2005. Over the years, the Company solidified its presence in the Visa and also ventured into providing E-Government services and Business correspondence services.

This segment of Business Correspondence and E-Government Services is now being spun off by the parent BLS International Services in the upcoming IPO of BLS E-Services Ltd.

BLS E-Services IPO Review

This Company is coming up with its BLS E-Services IPO Review the issue of Rs. 310.91 Cr which will open on 30th January 2024. The issue will close on 1st February and be listed on the exchange on 6th February 2024.

So let us take some time to understand the business in-depth and then take a look at what opportunities in the BLS E-Services IPO Review. Then let us look at the Company’s financials and compare the Company with its peers before we conclude what we think about the Company.

About the Company

The Company is a technology-enabled digital service provider, providing Business Correspondence services to major banks in India, Assisted E-services, and e-government services at grassroots levels in India. The Company has a robust network of access points for the delivery of essential public utility services, social welfare schemes, healthcare, financial, educational, agricultural, and banking services enabling government-to-consumer (G2C) touch points.

BLS can provide seamless services across India via its 1016 BLS Stores and 97,018 BLS touchpoints. These points are mostly available in semi-urban, rural, and remote areas where internet penetration is low & citizens need assistance in availing of technology-enabled services.

The business correspondents segment of the business provides products and services like opening savings, recurring deposit accounts, cash deposits, withdrawals, remittance, transfer, and bill collection services, through its Subsidiaries, namely ZMPL and Starfin. The Company generates revenue from monthly commissions, transaction-based commissions, and Registration Fees. Further, it also provides point-of-sales services, ticketing services, and assisted e-commerce services.

Additionally, the Company facilitates the delivery of various e-governance initiatives of the State Governments in India by providing various information communication technology (“ICT”) enabled citizen-centric services (“E-Governance Services”) through its touchpoints.

Registration of PAN, Aadhar, property registrations, and other such services are provided here. BLS E-Services has entered into an MOU with the National e-Governance Division (“NeGD”) for agent-assisted delivery of a unified mobile application, for new-age Governance (“UMANG”) services into its digital platform, offering convenient access to E-Governance Services. For every service delivered, a transaction fee is levied, along with a fixed government fee. The transaction fee is apportioned, after distributing to BLS Touchpoint and the Company, per the pricing dynamics established in each district as per the contract.

About The Industry

As of FY23, India has become the world’s most populous country with 142 crore people. The country has experienced remarkable growth in wireless connectivity, reaching 114 crore subscribers, with an average monthly data consumption of 17 GB, a significant increase from the 42 crore subscribers and 0.1 GB per month in FY17.

Despite this connectivity growth, India ranks 105th in the E-Government Development Index, according to a United Nations survey. In 2006, the Indian Government initiated the National e-Governance Plan, encompassing 31 mission-mode projects across various domains. However, the plan faced challenges, including a lack of integration among government applications and databases, limited government process re-engineering, and underutilization of technologies like mobile and cloud.

To address this issue the Department of Administrative Reforms & Public Grievances (DARPG) formulated the National e-Governance Service Delivery Assessment (NeSDA) in 2019. In 2021, the framework covered G2C & G2B services across Finance, Labour, Education, Local Governance, Social Welfare, Environment and Tourism.

As of FY23, the state Governments have stepped up to provide around 15,601 E-Services across the country. Madhya Pradesh provides the highest number of services at 936, followed by Karnataka at 866. Business Correspondents like BLS E-Services have entered the play by engaging with multiple banks to expand operations in towns & villages. As per RBI guidelines, at least 25% of the total banking outlets opened in a year must be in unbanked rural areas.

It also states that a Banking Outlet is a fixed point service manned either by the Bank’s staff or business correspondent. This has led to the rapid growth in the Business correspondent network in India which increased from 11.9 Lakh in FY21 to 22.1 Lakh in FY22.

The BC industry is currently growing at a CAGR of 19% from FY22 to FY25. Banks can cut operating costs as well as keep up with the RBI guidelines by partnering up with these BCs to open banks on their behalf in rural areas. Now that we have understood the industry in brief let us now look at how the Company performs financially.

BLS E-Services IPO Review – Financials

The Company has scaled its Net Revenue from Rs. 98.4 Cr in FY22 to Rs. 246 Cr in FY23, growing by a phenomenal 150%, and has scaled at a rate of 94% CAGR in the past 3 years.

During the same period, the Net Profits of the Company skyrocketed by 279%, from Rs. 5.37 Cr in FY22 to Rs. 20.33 Cr in FY23. Since FY21, the Company’s Net Profit has increased at the rate of 155% CAGR.

Net Profit Margins of the Company were at 8.36% as of FY23, which has expanded from 5.56% in FY22. This is what led to the 279% jump in Net Profits.

Return on Equity & Return on Capital Employed in FY23 remain strong at 33.33% and 30.62% respectively. Debt to Equity was at a high of 1.14x in FY21 and has reduced to 0.07 as of September 2024.

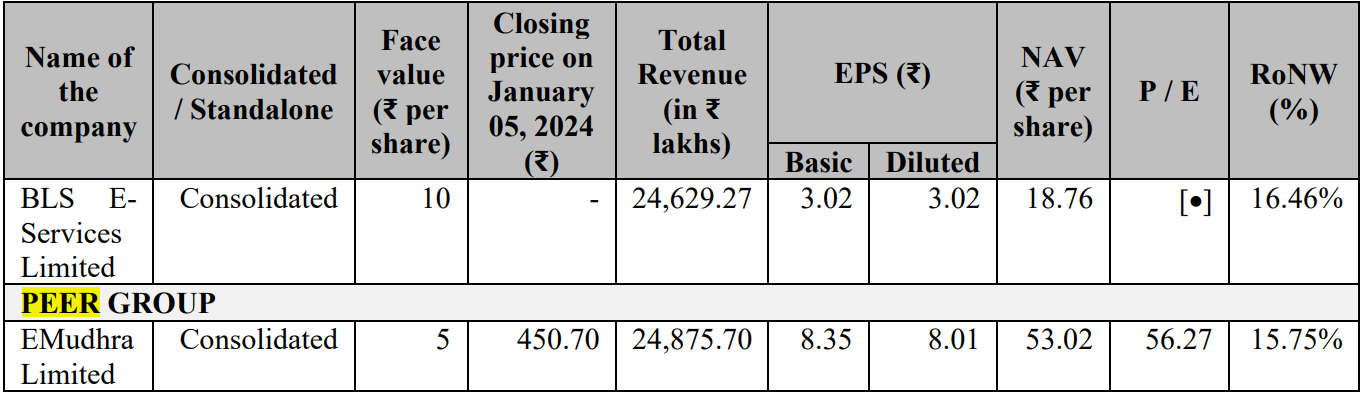

Key Players

The Company has only one listed peer which is E-Mudhra Ltd, which is a licensed authority which is involved in issuing digital signature certificates under the e-Mudhra brand. Both Companies have a nearly matched size by revenue, with E-Mudhra reporting higher Earnings Per Share of Rs. 8.35 as compared to the BLS’ Rs. 3.02.

If we take the higher end of the price band of BLS of Rs. 135 and calculate its IPO Price-to-earnings ratio, the Company has a PE ratio of 44.7x. This is however significantly lower than EMudhra’s PE of 56.27x. Nevertheless, when E-Mudhra filed its RHP, the Company had a Basic EPS of Rs. 2.49 as of FY21. At its highest Price Band of Rs. 256, the Company was valued at a PE of 103x and this IPO has given 75% returns to shareholders since listing in June 2023.

Strengths of the Company

- Asset Light Business Model: The Company operates on a franchise model where its merchants operate the BLS touchpoints, which are owned or leased by the merchants. BLS only provides access to its technological infrastructure.

- Multiple Cross-selling Opportunities: The Company recently launched the BLS Sewa App, a one-stop solution for multiple services like money transfers, recharges, demat account opening, air ticket booking, and a lot more.

- Negligible Acquisition Costs: The services provided by the Company are essential for the particular rural area. This way it has zero customer acquisition costs.

- Successful Acquisitions: BLS acquired Starfin India Pvt Ltd in August 2018 and Zero Mass Private Ltd. Both Companies contribute to 21% and 61% of BLS’ revenue respectively.

Weaknesses of Company

- Dependance on Commission: The Company predominantly earns from the fee & commission it charges its consumers. The rate charged is decided upon agreement with the state government, adverse effects to this can significantly disrupt the Company’s earnings.

- Dependance on Promoter: It is important to note that all the E-Governance projects are awarded to the Company’s promoter BLS International and not BLS E-Services, which is responsible for 28% of its revenue.

- Revenue Concentration Risk: With the slew of Acquisition of banking partners, the Company’s revenue generated as a Business Correspondent has increased significantly from 27.84% in FY21 to 66.05% of revenue as of September 2023.

- Customer Concentration Risk: The Company derives ~60% of its revenue from a single customer, a large PSU Bank. Additionally, the Company does not have any long-term agreements with the bank to count on.

BLS E-Services IPO Review – GMP

The shares of BLS E-Services Ltd traded at a 74.07% premium in the grey market on January 24th, 2024. The shares in Grey Market traded at Rs 235. This gives it a premium of Rs 100 per share over the cap price of Rs 135.

Key Information

Promoters: BLS International Services, Diwakar Aggarwal and Shikhar Aggarwal

Book Running Lead Manager: Unistone Capital Pvt Ltd

Registrar to the Offer: KFin Technologies Ltd

The Objective of the Issue

- Strengthening its technological infrastructure and developing new capabilities on its existing platforms

- Funding initiatives for organic growth by setting up BLS Stores

- To make further acquisitions and grow inorganically

- General Corporate Purposes

Conclusion

BLS International Services initially found itself a strong niche in the visa processing business nearly two decades ago. Ever since then, the Company has successfully developed its proprietary business and has also managed to build out another niche, which is the business correspondence business.

The parent company seems to have a great ability to find niches where it can operate as an informal monopoly and manage to build profitable and scalable businesses out of it. Now the parent company is spinning one such niche, BLS E-Services in this upcoming IPO.

This Company has been on an acquisition spree growing inorganically in the past three years. This has allowed the company to report margins in the triple digits. However, while it grew inorganically it has also maintained respectable margins & returns. Do you think it will go on to give multi-bagger returns like its parent company? So would you be applying for this IPO? Let us know in the comments below.

Written by Nasir Hussain

By utilizing the stock screener, stock heatmap, portfolio backtesting, and stock compare tool on the Trade Brains portal, investors gain access to comprehensive tools that enable them to identify the best stocks, also get updated with stock market news, and make well-informed investments.

Start Your Stock Market Journey Today!

Want to learn Stock Market trading and Investing? Make sure to check out exclusive Stock Market courses by FinGrad, the learning initiative by Trade Brains. You can enroll in FREE courses and webinars available on FinGrad today and get ahead in your trading career. Join now!!

[ad_2]